Insights + interviews

Post-retirement planning and living in Singapore

Post-retirement living in Singapore is not just about enjoying the fruits of one’s labor; it’s about navigating a new phase of life with its unique challenges and opportunities.

Singaporeans are living longer than ever before. As of 2022, the average life expectancy at birth in Singapore was 83 years. This longevity, while a testament to the country’s excellent healthcare system, also means that Singaporeans need to plan for a longer retirement period.

The number of senior residents aged 65 years and over in Singapore grew from 338,000 in 2010 to 614,000 in 2020. As of 2020, seniors formed 15.2 per cent of the resident population, an increase from 9.0 per cent in 2010.

This demographic shift has significant implications for retirement planning and the quality of life in the post-retirement years.

Quality of Life in Retirement

Maintaining a specific quality of life in retirement is a common expectation among Singaporeans. A report found that people in Singapore aged 65 and above and living alone need about SGD 1,379 a month to meet basic standards of living. However, despite being top in the world for retirement finances, Singapore ranks lower for retirees’ quality of life.

Many Singaporeans expect to work after retirement, with 51 percent planning to do so to preserve their health and wealth. Furthermore, 78 percent of Singaporeans underestimate the retirement amount needed based on their ideal retirement style.

We had a discussion with Raymond Ong, CEO of Etiqa Insurance Singapore about post-retirement planning, what does it entail, why is it required, and how can we start the process.

the Active Age (AA): What does retirement planning entail?

Mr. Raymond Ong (RO): Retirement planning has been perceived as challenging, as revealed by the results of the Etiqa Insurance Singapore’s 2022 Retirement survey where 44 percent of respondents revealed low confidence in retiring comfortably. Ensuring a secure retirement entails significant forward planning.

The first step is for individuals to start as early as possible. Starting retirement planning early offers the advantage of being able to allocate smaller sums towards the retirement goal, as opposed to requiring larger sums or larger percentages of income if the retirement planning is delayed. By starting early, the impact of compounding helps to build a more comfortable retirement nest egg while pursuing their life experiences.

Furthermore, being young means that one can take on more risk, or invest in longer term investments, which is expected to produce higher returns (although this may come with greater volatility).

The next step is to save regularly. A good starting point can be as simple as setting aside a fixed amount from each paycheck into a retirement savings account. However, a comprehensive retirement strategy may also include using appropriate investment vehicles to accumulate the necessary funds.

Individuals also need to forecast how much money they will need to have a comfortable retirement. Given the diversity of expectations and goals, there is no one-size-fits-all approach, making it crucial for individuals to first identify the lifestyle that they want to live post-retirement. Future expenses such as holidays, medical bills, health insurance premiums and their current financial standing must also be taken into consideration when setting realistic savings goals.

Additionally, individuals should factor in inflation to ensure that their retirement savings goals will be able to sustain them through the rise in cost of living. With Singapore’s inflation reaching up to 4.8 percent, the cost of living has also gone up significantly, putting increased financial burdens on everyone. It is thus, crucial to manage finances more strategically and plan for retirement early to build a financial safety net that helps them weather economic downturns and unexpected expenses as they grow older. Having a personal retirement plan, in tandem with existing government schemes such as CPF, will ensure one has comprehensive financial protection in their later years.

Finally, individuals should purchase protection insurance to safeguard this savings. Rather than tapping on your retirement savings when faced with accidents or unforeseen events, a prudent choice is to shield your hard-earned savings from potential depletion due to unexpected expenses like medical bills, disability costs, or loss of income. Protection insurance acts as a financial buffer against these disruptions, ensuring the security of your financial future.

AA: Why is this important for the individual and for the family?

RO: Retirement planning is crucial for both the individual and their family due to several factors.

For the individual, retirement planning serves as a crucial tool for building financial security. The accumulation of savings and investments during one’s working years will provide a reliable income stream after retirement, empowering the individual to meet daily expenses, healthcare needs, unexpected expenses. This, in turn, decreases the likelihood of the individual becoming a financial strain on their family, preventing potential financial burdens on family members and contributing to the overall financial stability of the family at the same time.

Financial reasons aside, retirement planning also affords the individual the opportunity to live a comfortable and fulfilling post-retirement life. Having the financial capability to maintain or enhance their desired lifestyle, support continuous learning, and fulfil personal goals, travel aspirations, and leisure activities are benchmarks of a secure retirement. Moreover, it enables a smooth transition into retirement for not just the individual but also the family. Having a solid retirement plan in place will minimise any stress and uncertainties associated with sudden lifestyle adjustments or unexpected expenses, fostering a more harmonious family environment.

In essence, retirement planning is a crucial step in life that not only secures the individual’s financial future but also contributes significantly to the overall stability and well-being of the family unit.

AA: How does having a retirement plan set one up for their future, and help to provide stability in the present?

RO: A well-structured retirement plan involves a systematic approach to accumulating savings and investments throughout an individual’s working years. By consistently setting aside funds and strategically investing them, the individual will have a financial reservoir that can be tapped into during retirement. Essentially, retirement planning sets up a financial safety net that enables individuals to approach their retirement years with confidence and pursue their interests and desires without financial constraints.

The presence of a well-thought-out retirement plan itself significantly contributes to present stability – the assurance of having a roadmap for the future helps alleviate financial stress and anxiety. Having a disciplined savings and investment routine, coupled with the inclusion of protection insurance, better equips individuals to effectively manage their current financial responsibilities and handle any unforeseen expenses, for example, due to accidents. This sense of financial security translates into peace of mind, which consequently contributes to a more stress-free present and improved quality of life.

AA: Where should an individual start from when it comes to retirement planning?

RO: Firstly, it is imperative for individuals to determine their investment approach – whether it involves a lump sum allocation or regular contributions. This decision should align with one’s financial goals and capacity for consistent investments. They should also consider their risk appetite and time horizon, which determines how comfortable one is with market fluctuations and specifies the duration for which they can commit to their investment goals.

More importantly, individuals need to distinguish between immediate financial needs and long-term retirement savings. Identifying and segregating short to medium-term financial requirements from long-term savings ensures that the funds allocated for retirement remain untouched.

With those considerations in mind, one can then plan to close his/her savings gap to accumulate sufficient funds for retirement. Based on one’s projected retirement lifestyle, make a monthly budget to determine how much is needed per month after retirement. As a guide, one can factor in inflation and expected investment returns to estimate how much is needed to retire comfortably.

The next step is to choose investment vehicles to build up your retirement nest egg. The Central Provident Fund (CPF) and Supplementary Retirement Scheme (SRS) are examples of retirement schemes that allow individuals to invest their contributions and save up for retirement. Whether savings take the form of fixed deposits or bonds, there is no one-size-fits-all approach to structuring and investing your savings for retirement. But as a rule of thumb, it is crucial to sufficiently diversify one’s retirement portfolio, spreading your investments among different types of assets to reduce overall risk.

In cases of uncertainty, seeking the guidance of a financial advisor is extremely helpful. A financial advisor can conduct a thorough assessment of the individual’s need and provide personalised insights and recommendations to navigate their financial decisions.

Finally, one must periodically review and adjust his/her retirement plan in accordance with the evolving economic landscape. Economic factors, such as inflation and market conditions, and personal factors, like major life events or milestones, significantly affect the success of your plan, hence it is good to regularly assess and adjust it to ensure its effectiveness.

AA: How does the financial environment (slow economy, rising inflation, etc) impact one’s retirement plans?

The financial environment holds a significant influence over one’s retirement plans. In a slow economy scenario, the impact on retirement plans can be twofold. Firstly, diminished investment returns due to subdued market conditions can affect the growth of one’s retirement savings. Secondly, job security and income streams may become major concerns. In such times, individuals should reassess their investment strategies and look to fortifying their emergency funds to navigate any potential job-related uncertainties.

As for the case of rising inflation, individuals may struggle to keep up with saving for retirement on top of current financial responsibilities. With the rising cost of living, individuals need to reassess their retirement savings goals to address both immediate and future financial considerations.

AA: What are some tips to bear in mind when looking and managing a retirement plan for yourself?

RO: There are several tips that one must keep in mind when doing a retirement plan.

- Starting early: Starting your retirement planning journey early and setting aside regular savings as a habit provide substantial advantages, such as compounding. Your invested fund will have more time to grow, which will potentially yield greater returns over the long term and allow you to reach your retirement savings goals. This proactive approach also helps you to defray the escalating cost of health insurance premiums in your retirement years, which tends to rise with age.

- Diversifying investments: Diversification is a fundamental principle in effective retirement planning. Rather than putting all your eggs in one basket, spreading your investments across a variety of asset classes can help mitigate risks and enhance potential returns. One can consider a mix of stocks, bonds, investment-linked policies (ILPs) and other vehicles of investments that align with their risk tolerance and financial goals.

- Staying informed: Keeping yourself well-informed about changing regulations that may affect how you invest, financial markets and economic trends enables you to make informed decisions as well as adapt to economic changes, ensuring that you optimise your retirement plan based on the current financial landscape. Changes to the CPF scheme for example, may also affect your investment.

- Staying protected: Getting protected from any unforeseen events or accidents can safeguard your retirement savings and ensure a resilience and stable financial future.

- Regular review and adjustment: Reviewing one’s financial plans periodically are also a crucial step in retirement planning. Life circumstances, financial goals and market conditions change over time, so it is important for one to periodically reassess their retirement plan to ensure it remains aligned with their needs. Regular reviews and informed adjustments will allow your retirement plan to stay on course for long-term success.

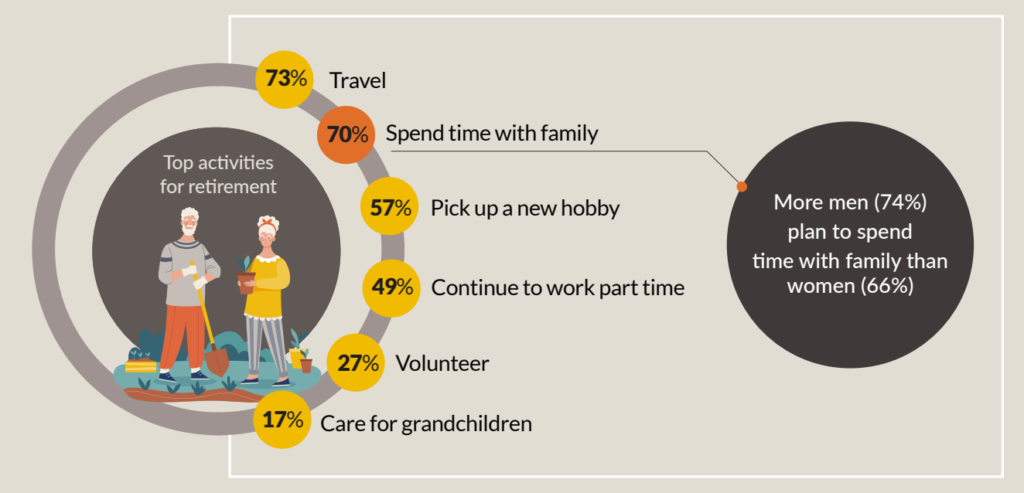

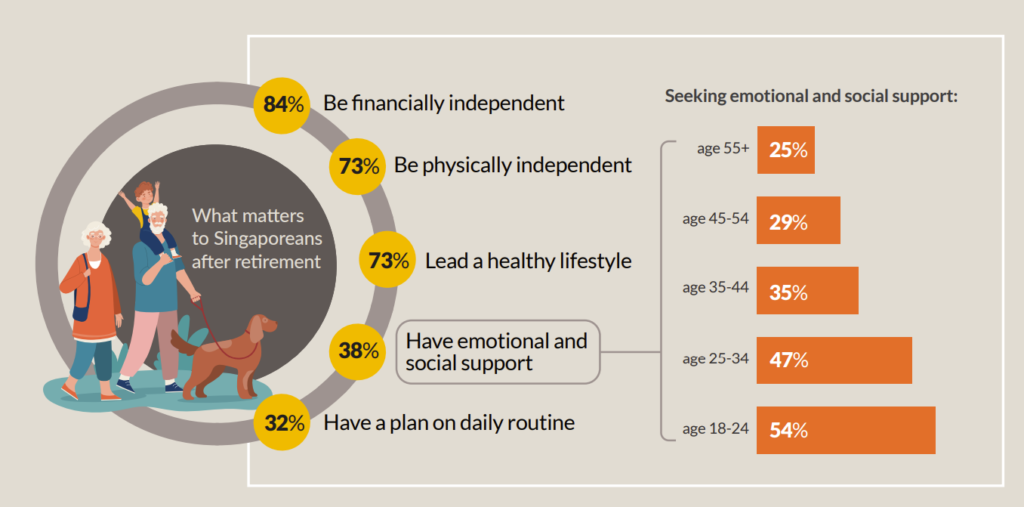

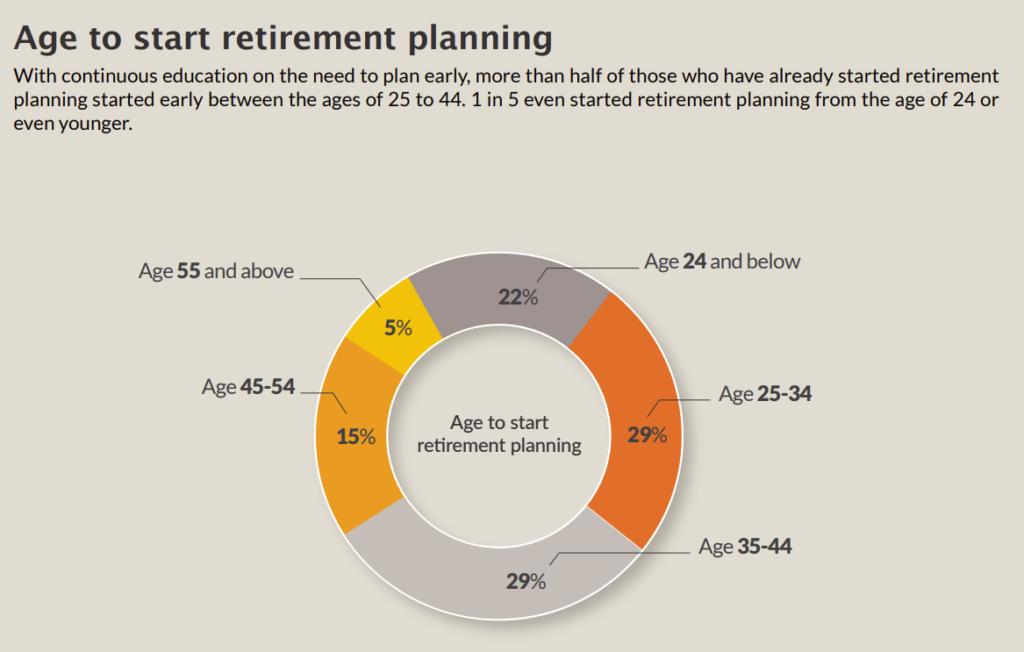

Graphics and data attributed to Etiqa Insurance Singapore’s 2022 Retirement survey.

Photo by Andrew Neel and by Harli Marten on Unsplash

{kind=link}