Insights + interviews

Singapore Posts Largest Decline In Financial Literacy

MasterCard’s latest Financial Literacy Index show that progress has stalled in region with 12 of 16 countries recording lower scores in financial literacy.

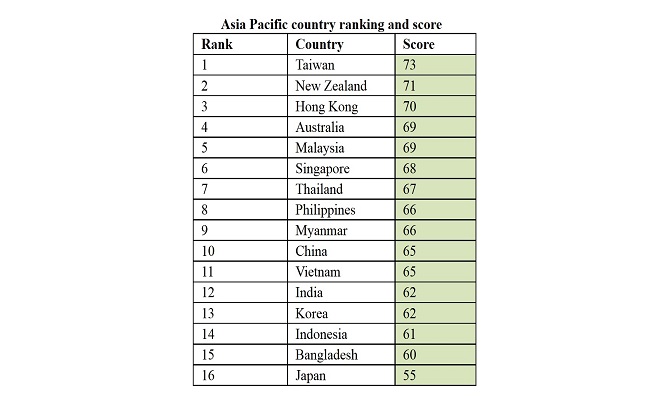

MasterCard has revealed that Singapore has fallen to sixth place for financial literacy*, recording the largest decline out of 16 Asia Pacific markets. Singapore was previously ranked second in the region, sliding four index points to score 68 index points in financial literacy.

*Financial literacy or fin-lit is the understanding of financial matters. Fin-lit often entails the knowledge of making proper decisions pertaining to certain personal finance areas like real estate, insurance, investing, saving, tax planning and retirement.

The struggle to improve financial literacy is taking place throughout the region. Data from the MasterCard Financial Literacy Index showed that progress towards improving basic finance knowledge and skills across Asia Pacific has stalled as 12 of 16 countries record lower scores in financial literacy. While Singapore’s ranking saw the biggest decline, the survey showed generally disappointing results in developed markets (Australia, Japan, New Zealand, Singapore, South Korea and Taiwan).

With an overall Financial Literacy Score of 73, Taiwan’s advancement of 2 points places it in first place in the Asia Pacific, allowing it to regain top spot after dropping to third place in the previous survey. Hong Kong’s advancement from fifth place in Asia Pacific to third place overall is due to the decline in scores for the top few markets: Singapore (down 4 points to 68, with the biggest drop regionally regressing from 2nd to 6th place in the region), New Zealand (down 3 points to 71), Australia and Japan (down 2 points to 69 and 55 respectively).

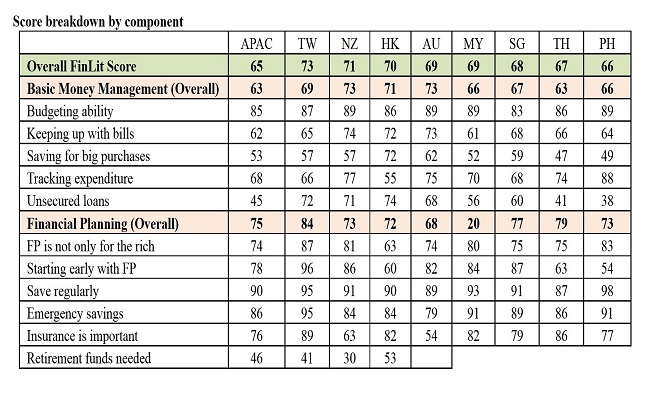

In Singapore, the key reason for the overall decline in financial literacy seems to be a fall in consumers’ understanding of basic money management with this component falling almost six points. Going by the survey results, people in Singapore are finding it harder to keep up with bills, budget effectively and manage unsecured loans.

“Crucial to improving financial literacy is encouraging education at an early age. A practical understanding of how to manage money, including saving and borrowing, should be provided by parents and taught at school. The goal is to eventually develop financial know-how so that people can effectively manage money matters such as household cash-flows and loans,” said Deborah Heng, group head and general manager, MasterCard Singapore.

All seven developed markets (including Singapore) have not yet achieved gender parity in financial literacy, although in Japan, women are one point shy of achieving this compared to their male counterparts. In second place for gender parity amongst the developed markets was Taiwan, while Singapore, Hong Kong and Australia tied for third place followed by New Zealand and South Korea. Comparing gender parity scores to data from a year ago shows that there is in fact a widening gap between the sexes in financial literacy scores. Taiwan was the only market where improvement was seen, while all other markets declined by between one and six points.

T.V. Seshadri, Group Executive, Global Products and Solutions, MasterCard Asia Pacific said, “There is no one reason for the falling level of financial literacy across the region but the data clearly shows that the young and unemployed need additional support. Educating people so they can plan for the future is a crucial aspect of financial inclusion. In both developed and emerging markets, people are struggling to understand basic financial concepts such as inflation. In addition, while Asia Pacific is a region of savers, the lack of retirement planning should cause particular concern. It is not enough to provide access to financial services, we must ensure that everyone knows how to save, budget and invest so that their wellbeing can be secured over the long term.”

The 4th MasterCard Index of Financial Literacy is calculated out of the weighted sum of the 3 components: Basic Money Management (50% weight) which examines respondents’ skills with regards to budgeting, savings, and responsibility of credit usage; Financial Planning (30% weight) which assesses knowledge about financial products, services, and concepts, and ability to plan for long-term financial needs; and Investment (20% weight) which determines respondents’ basic understanding of the various risks associated with investment, different investment products and skills required. 8,087 respondents aged 18-64 in 16 countries in Asia Pacific were surveyed between July and August 2014 (Australia, New Zealand, China, Hong Kong, Taiwan, Japan, Korea, Malaysia, Philippines, Thailand, Indonesia, Singapore, Vietnam, India, Bangladesh, and Myanmar). In Singapore, approximately 500 respondents participated.

Top findings:

- Taiwan regains top spot followed by New Zealand (which drops from 1 Kiwis and Taiwanese over 30 years old the most financially literate in the region.

- Singapore goes from 2nd to 6th place, with the biggest drop in score regionally.

- While developed markets tend to rank higher than emerging, Japan remains the outlier staying in the bottom spot for the 3rd consecutive year.

- Among the emerging markets, India advances the most, gaining 3 points to 62, placing it at 12th place in the region (16th in APMEA), and nearly at par with South Korea (62 points, rank 13 regionally).

- China is top overall in ‘Investment Know-How’ but among the worst in ‘Basic Money Management.’

- Asia Pacific is a region of savers with the majority of people knowing how to ‘Budget’ and ‘Save Regularly.’ However, knowledge of ‘Retirement funds needed’ is low in both developed countries and emerging markets.

- Knowledge of the risks associated with investment is poor across the region with the concepts of ‘Inflation’ and ‘Diversifying assets’ particularly badly understood, especially in emerging markets.

- The financial literacy gender gap is higher in developed markets (excluding Taiwan) than emerging markets. The gender parity gap in South Korea is the widest, followed by Hong Kong and Australia.

- In terms of age, people under 30 are less financially literate than those over 30 in all markets. With regards to employment status, with the exception of India and Bangladesh, people who are “Working” have superior financial literacy skills than those “Not Working.”

- Aside from Taiwan and India, Vietnam and Indonesia are the only markets to improve their score in 2014 than 2013.Issue specific insights

- Taiwanese Financial Planning Savviness Shines – Results from recent research conducted by Manulife suggest that 7 out of 10 Taiwanese investors are not confident that their mandatory pensions will be sufficient to cover their retirement expenses. This lack of confidence and know-how may be prompting the Taiwanese to be active and prudent savers (score for both “Save Regularly” and “Emergency Savings” is very high at 95). In fact, data from Directorate General of Budget, Accounting and Statistics Taiwan (DGBAS) show personal savings in Taiwan to have increased by 9.96% (1424600 TWD Million to 1582300 TWD Million) from 2011 to 2012 .

- Myanmar: Prudent Savings, Growth of Insurance Sector Earmarked to Accelerate – Myanmar continues to score consistently higher than most of its regional peers in the savings and insurance-related categories of Financial Planning with a score of 81, placing it in the top 3. This could be due to the lack of social security benefits in the country, which has in turn inculcated a practice of prudent savings for costly essentials like healthcare, education and emergencies. The results also show the Burmese to have high regards for insurance. This trend is likely to remain strong, in view of the recent ending of the government-owned company Myanmar Insurance’s 60-year monopoly of the country’s private insurance industry. This milestone reform will not only allow private and foreign insurance companies to enter the market, but will be beneficial to Burmese consumers through heightened awareness of both life and general insurance concepts and products.

- Japan’s lack of progress in Basic Money Management – Japan’s score has been steadily declining since the survey was first launched and the latest results indicate further deterioration in money management skills. This is likely attributed to the country’s aging population and stagnant income growth. Currently the world’s oldest country, Japan’s aging population are now the biggest spenders of their savings and retirement funds. OECD figures show that compared to its G7 peers, Japan’s household savings rate is 0.6% of disposable household income, a stark contrast to other countries such as Australia (9.3%) and South Korea (5.3%).

- Explaining the gender gap – Across the 16 regional markets, the gender disparity gap is most pronounced in the six developed markets (excluding Taiwan). In contrast, the difference in financial literacy scores is only slight in countries such as China, India, Indonesia, Malaysia, Vietnam and Bangladesh. The gender gap in developed markets could be due to the diminished amount of time afforded to day-to-day budgeting and tracking of expenditure with increased work responsibilities. The reason why women in emerging markets have more similar scores to men may be because financial systems are at infancy stage so women and men are more likely to be equally aware and informed. It may also be because income level is lower on average, making it necessary to be even more conscious of money and track expenditure on a regular basis.

{kind=link}